At A Glance

Fast takeaways for decision-makers.

- 1Providing clear and accurate information about the products and services that they offer so that consumers can make informed decisions about whether these products and services are suitable for their needs.

- 2Responding promptly and effectively to complaints from consumers, and providing customers with a fair and unbiased resolution to any issues that they raise.

- 3Ensuring that financial products and services are designed and sold in a way that is fair and transparent and that customers are not misled or unfairly disadvantaged by the way in which these products and services are marketed or sold.

The FCA Consumer duty is a key principle of the regulatory framework that governs the financial sector in the UK. This principle requires financial firms to always act in the best interests of their customers and to put the interests of consumers first when carrying out their activities.

What is the FCA Consumer duty?

Consumer duty was introduced as part of the FCA's broader strategy to improve the way that complaints are handled within the financial sector and to ensure that consumers are treated fairly. This duty complements other key principles of the FCA's regulatory framework, such as the requirement for firms to act with integrity and the requirement for firms to manage conflicts of interest in a fair and transparent manner.

In this article, we will explore the FCA Consumer duty in more detail, and we will look at the key requirements that financial firms must meet in order to comply with this principle.

We will also look at the role that the FCA plays in enforcing the FCA Consumer duty, and we will consider some of the challenges that firms may face in meeting their obligations under this principle.

The requirements of the FCA Consumer duty

In order to comply with the FCA Consumer duty, financial firms must take a range of steps to ensure that they are meeting the needs of their customers and that they are providing them with the best possible service. This includes:

- Providing clear and accurate information about the products and services that they offer so that consumers can make informed decisions about whether these products and services are suitable for their needs.

- Responding promptly and effectively to complaints from consumers, and providing customers with a fair and unbiased resolution to any issues that they raise.

- Ensuring that financial products and services are designed and sold in a way that is fair and transparent and that customers are not misled or unfairly disadvantaged by the way in which these products and services are marketed or sold.

The Consumer duty also applies to the way that financial firms deal with vulnerable customers. This means that firms must take extra care to ensure that they are providing these customers with the support and assistance that they need, and that they are not taking advantage of their vulnerability in any way.

Overall, Consumer duty is an essential part of the regulatory framework that governs the financial sector in the UK. By requiring firms to always act in the best interests of their customers and to put the interests of consumers first, the FCA helps to promote trust and confidence in the financial sector and to ensure that consumers are treated fairly and with respect.

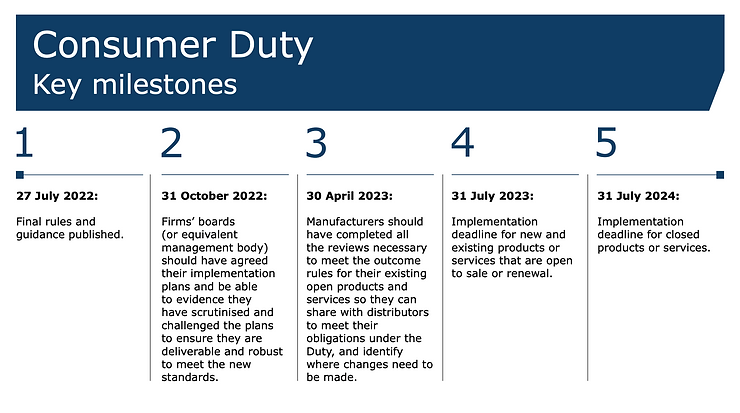

Timelines

Below are the key Consumer Duty timelines you need to be aware of.

About MEMA

Our specialist team has the experience and expertise to help you. Our offering includes a regulatory business plan, a suite of compliance policies and procedures, and an IT security risk assessment. We can provide template documents and work with you to tailor these to your specific circumstances. We can also carry out a gap analysis on your current policies and procedures – and help you address any action points identified.

We will explain to you the FCA’s expectations and its recent publications and prepare a gap analysis and/ or a suitable remediation plan. Among the firms, we work with are:

- Payment initiation service providers (PISPs)

- Account information service providers (AISPs)

- E-Money institutions

- FX exchange companies

- Merchant acquirers

- Bill payment service providers

- Electronic communication exclusion businesses

If you need any help or would like a complimentary chat select the button below.