At A Glance

Fast takeaways for decision-makers.

- 1provide your customers with a fee illustration for each of the redress bands

- 2ensure that your fees are reasonable in cases where fees charged on non-PPI financial products and services claims are outside the scope of the cap

- 3make clear to consumers where relevant that they may need to pay a CMC fee out of other funds

- 4disclose key information to consumers at the pre-contract stage, to help consumers make better-informed decisions about using your services

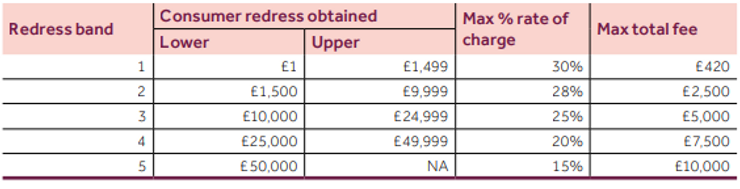

You will be aware that the FCA’s price cap is coming into existence on 1 March 2022.

As a quick primer, this means there will now be five redress bands with a maximum fee charged per band.

What are some of your requirements:

The fee cap requires your firm to

- provide your customers with a fee illustration for each of the redress bands

- ensure that your fees are reasonable in cases where fees charged on non-PPI financial products and services claims are outside the scope of the cap

- follow existing rules (CMCOB 6.1.7) to promptly give customers an estimate of the fee they will pay at the point your firm has sufficient information to reasonably estimate the fee, and, if applicable, to tell customers why the fee payable will differ from the illustration

- make clear to consumers where relevant that they may need to pay a CMC fee out of other funds

- provide illustrations within each fee band applicable to your customer and test and adapt communications aligned to this fee band. In instances, where your customers are likely to have redress that is not paid out to them in cash, it is preferred that you help them understand the fees they will pay in those circumstances

- disclose key information to consumers at the pre-contract stage, to help consumers make better-informed decisions about using your services

What to remember

- The cap will not apply to pre-existing contracts unless the contracts are varied to increase fees or add new fees and

- where new claims are added to the contract or the customer did not authorise or instruct your firm to act in relation to the claim until after the rules came into force (in which case, the new claims will be subject to the cap).

- The FCA will be monitoring the effectiveness of the fee cap via your regulatory returns and its ongoing supervisory work.

- The FCA will also consider whether fees are clustered under the level of the cap and whether, in addition to complying with the cap, your firm is treating customers fairly under Principle 6 and CMCOB 2.1.1R. Essentially are you only charging the maximum fee per band and is this appropriate on a business and consumer level?

MEMA

MEMA is supporting a number of clients in fee cap readiness and if you are interested in a conversation on what steps you require do reach out to us.